Chief Executives’ Group – North Yorkshire and York

17 September 2021

Economy Update and Plan for Growth

1. Purpose of the report

1.1 To provide an update on the state of the economy.

2. How well are North Yorkshire and York recovering?

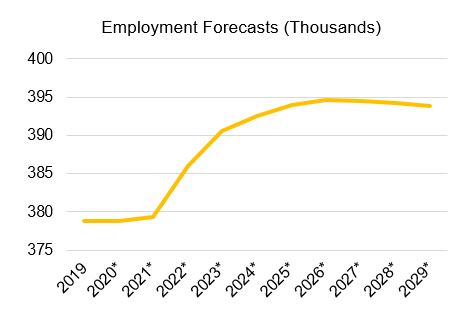

2.1 Employment forecasts for York and North Yorkshire are incredibly resilient compared to previous estimates. In December, pre-Covid levels were anticipated to return by 2025. This was then bumped up to 2022 in April forecasts, but now, according to Oxford Economics, employment will recover this year. In fact, it was estimated that only a minor dip (-0.02%) was experienced within 2020.

2.2 Sectoral differences are apparent within the forecasts. Accommodation and Food Services and Manufacturing are not anticipated to return to pre-Covid levels, even by 2029. Comparatively, in 2021, demand has grown across many other sectors, including: Administrative and Support, Human Health and Social Work, Other Service Activities[1], and Public Administration and Defence, to name a few. Mostly, these are the sectors that have been able to easily adapt throughout the pandemic.

2.3 However, this growth could face blockages, particularly in social care. Stakeholders have reported that the sector is at a crisis point. There’s already staff shortages due to a lack of migrant workers, but policies around vaccines may limit the availability further. If carers have not had the two vaccines, they won’t be able to work in social care. There are still a significant number of employees in this sector that won’t get the jab – not only could this create shortages, but it could lead to unemployment for some.

(Sectoral differences are explored further in section 2)

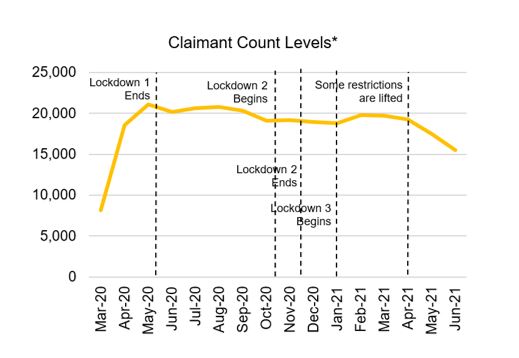

2.4 Claimant count levels: the pandemic had an immediate impact on claimant count levels and has remained substantially high throughout 2020. Reassuringly, the numbers are now starting to decrease and have continued to decline from February 2021 to June 2021. However, levels still remain 89% higher than pre-Covid figures.

Source: Office for National Statistics

*The experimental Claimant Count consists of claimants of Jobseekers Allowance (JSA) and some Universal Credit (UC) Claimants. The UC claimants that are included are 1) those that were recorded as not in employment (May 2013-April 2015), and 2) those claimants of Universal Credit who are required to search for work, i.e. within the Searching for Work conditionality regime as defined by the Department for Work & Pensions (from April 2015 onwards).

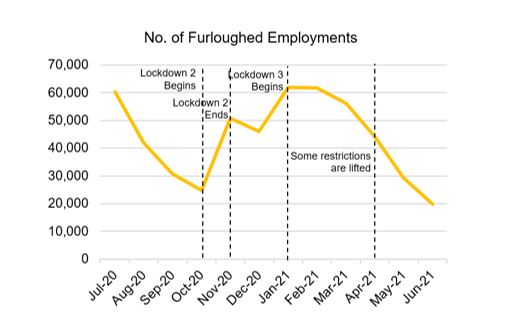

2.5 Job retention scheme; The level of furloughed employments has decreased since restrictions began to be lifted in April 2021. Previous employment forecasts were based on the level of furlough and assuming that these jobs were most at risk. However, we have not yet seen any massive drop-offs in employment. In 2020, the unemployment rate remained incredibly low at 2.3%.

Source: HMRC

2.6 The sectors with highest remaining furlough levels are Accommodation and Food Service (9,950), Wholesale and Retail (3,750) and Manufacturing (2,720). These are traditionally the lower paid jobs and there is some concern that those on furlough will have moved into alternative, lower risk, sectors which is resulting in a workforce shortage as businesses look to reopen.

2.7 The Self-Employment Income Support Scheme (SEISS) had 22,500 claims within July, a minor decrease from the previous month. Although these government support packages have been invaluable, research from Simply Business revealed that 81% of self-employed people felt it hasn’t been enough and over two million SMEs across the UK have been unable to access any financial support[2].

2.8 Towns: vacancy rates for retail and leisure were approximately 9.2% in July 2021 for York and North Yorkshire; a minor increase from 12 months ago. A similar pattern can be seen across some of our key settlements, with very few experiencing a noticeable change.

Source: Local Data Company

3. Where and for whom is recovery not happening (with a focus on equality, diversity and inclusion issues)?

Hospitality

3.1 Undoubtedly, hospitality has been one of the hardest hit sectors during the pandemic. According to the ONS, hospitality saw signs of recovery in spring 2021 with consumer spending increasing, but business confidence still remains low, and there are ongoing challenges for the sector.

3.2 Sub-sectoral differences are also apparent, with food and drink businesses estimated to have lost more than double the money of the average small business[3].

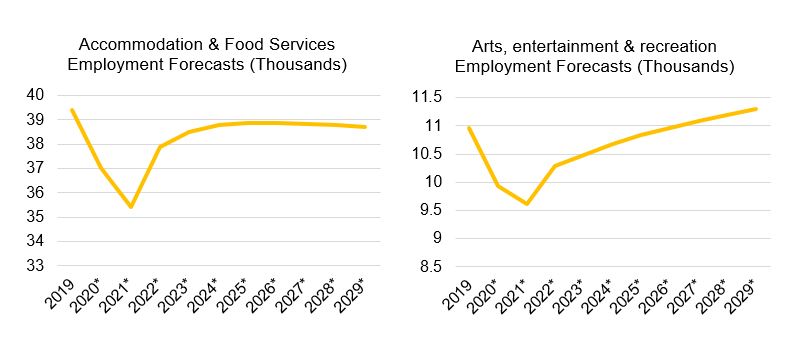

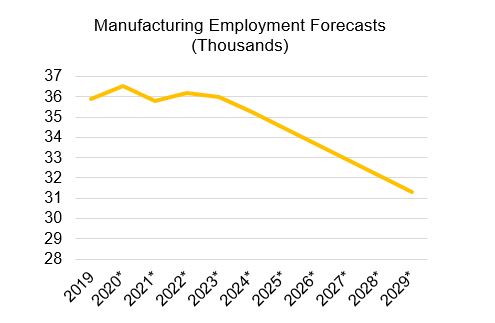

3.3 Employment forecasts for hospitality and tourism reflect the vulnerability of these sectors during the pandemic, compared to other industries. Accommodation & food services remained unchanged from previous forecasts, with pre-Covid levels still not anticipated to return, even up to 2029. Interestingly, arts, entertainment & recreation has a slower recovery than previously forecasted.

3.4 Staycations may have provided a boom for the sector, but there are a number of constraints that have limited this opportunity. For example, social distancing requirements mean lower capacity within restaurants/cafes, and shortages in staff due to the “pingdemic”.

Source: Oxford Economics (July 2021)

3.5 The SWOT analysis outlines some of the high level challenges and opportunities that this sector is facing and may provide some rationale for the latest forecasts:

| Strengths | Weaknesses |

|

Consumer habits are changing: there’s a greater emphasis on local independents. As a result, multiple large chains have closed (Gap, John Lewis, Topshop) Staycation boom: many places are busy even if they are not a typical tourist location |

High levels of debt have been accrued throughout the pandemic and repayments will soon need to be made Limited opening hours due to a lack of staff Business models have changed: continental style (i.e. table service) has been provided, which means more staff are needed and less covers, but many haven’t increased their prices to match this demand Hospitality isn’t seen as a long-term career option |

| Opportunities | Threats |

|

Pent-up demand from consumers High levels of vacancies could provide employment opportunities for the wider workforce Challenge mind-sets around hospitality and demonstrate lifelong career opportunities |

Highly seasonal and all of the government support is reaching a cliff’s edge during this period Xmas parties and meals are essential for winter season – will demand exist for this? “Pingdemic”: staff are being forced to isolate when businesses are already at low capacity High levels of last minute cancellations from consumers Labour shortages – including a drop-off from younger people having weekend jobs Risk of being shut down again if Covid cases increase Staycation boom is short-lived and vacations abroad dominate in 2022 |

3.6 Labour shortages, both a result of recruitment and retention, are the biggest barriers right now, hitting at a time when most places are busier than ever. In York alone, there are more than 100 vacancies in eight hotels, particularly in the food and beverage and kitchen departments[4].

3.7 There is not an easy fix to resolve this challenge. Industry leaders at the York Hospitality Summit suggested the following solutions, which require both public and private sector intervention: flexible training (i.e. bootcamps) to help fill positions; employers need to change perceptions around life-long career opportunities; public transport for industry workers; and increases to wages.

3.8 The LEP Skills team are also exploring how the wider workforce can be matched-up into hospitality roles.

3.9 These challenges are not unique to York and North Yorkshire. Cumbria are facing a similar shortage and are lobbying government to introduce a new visa to fix the staffing crisis in this sector.

Manufacturing

3.10 Alongside hospitality, manufacturing has been one of the most disrupted sectors this year, both from Covid-19 and the EU transition. The latter plays out in the employment forecasts with Oxford Economics anticipating that changes to trade policy will lead to decreases in employment growth, alongside improvements to productivity via automation (which is already underway in businesses such as Nestle).

Source: Oxford Economics (July 2021)

3.11 The below SWOT analysis outlines the key challenges and opportunities that the sector is currently facing.

| Strengths | Weaknesses |

|

Demand is very strong for a lot of businesses right now |

Labour supply shortages: impacting on manufacturers’ ability to produce goods in the volumes and timeframes required Limited investment decisions: as conditions are still seen as volatile and unstable Businesses cannot grow or plan to grow without access to labour Cashflow is still a concern for many |

| Opportunities | Threats |

|

Increased shift to automation to increase productivity and high wage roles Rebuild supply chains with local businesses and identify new high demand products Good business charters: becoming more attractive as employers, i.e. better contracts, working times etc. to reduce turnover of staff Regional cross-working for affordable transport to large labour areas from deprived areas |

Staff shortages also within the supply chain, which is impacting ability to operate at full capacity Staff shortages become unsustainable for certain employers to remain in the region Challenges with getting goods into the country: both as a result of the pandemic and the resulting bottlenecks in international logistics Massive price increases on goods Shift to automation reduces job roles and there may not be the right available skills to manage this |

3.12 Again, labour shortages are a big restriction, but these are exacerbated further in the manufacturing sector due to the impact it is having on their supply chains. For example, there is a lack of drivers available to deliver their goods.

3.13 In response to this, the LEP launched a survey with the region's food and drink manufacturers. 36 manufacturers took part including the largest employers. Respondents were asked if there was any regional activity they would like to see to support labour shortages. The following were the most popular response themes in order:

a) Free or affordable public transport linking recruitment conurbations to industrial sites/ areas (many of the rural in YNY)

b) End furlough - get everyone back to work and free up the labour market

c) Improved tax relief for low skilled workers – linked to travel

d) Joined-up regional jobs advertising

e) Affordable housing for workers

f) National/regional push to make the Yorkshire Coast an attractive place to move for work

Debt levels

3.14 Informal feedback from business stakeholders indicates increasing concerns around debt levels, particularly amongst small and micro businesses. This reflects the ending of furlough support, coupled with the additional debt taken on during the pandemic, such as through the government backed loans, and inflationary pressure on raw materials and supplies driven by supply shortages. The LEP Growth Hub is working to provide support on these key issues.

Public sector

3.15 Labour shortages are not just apparent within the private sector; this is also reflected within the public sector. Local authorities have reported that there is both a lack of labour and skills within planning roles. Alongside this, there has been an influx of planning applications and a strong demand; the construction sector is booming. It is likely that uncertainty around Local Government Reorganisation is contributing to recruitment and retention issues.

4. Plan for Growth

4.1 Building on the evidence base, the Local Industrial Strategy and Covid recovery plan, the LEP is developing a York and North Yorkshire Plan for Growth. The purpose of a York and North Yorkshire Plan for Growth is to set the economic strategic framework:

- that builds on the agreed Local Industrial strategy and aligns others economic strategies across YNY

- that provides the basis for future funding bids to, and influence for, the Government's Shared Prosperity Funding and further levelling up funding.

- that sets out the next step in how York and North Yorkshire can recover and grow post Covid 19

- that enables partners and stakeholders to work together to achieve ambitious economic outcomes for York and North Yorkshire

- that helps to drive forward the economic agenda for the Devolution Deal, the new Local Government structure and proposed Combined Authority in YNY, and

- that clearly shows how YNY can make a significant contribution towards the Government's ambition for a Global Britain, Levelling up and Net Zero.

4.2 This plan will be developed in a way that:

- engages and aligns all workstreams across the LEP

- fully engages the LEP Board and Sub Boards and LA Directors of Development in the process

- seeks the views of stakeholders and gets their buy-in

- has a clear governance and ownership

The Structure and Framework

4.3 In developing this structure, the YNY Plan for Growth will identify three strategic objectives based on the national Plan for Growth ambitions which align to the York and North Yorkshire vision of a Greener (Net Zero), Fairer (Levelling up) and Stronger (Global Britain) economy. Building on previous plans and strategies, it is proposed that these are focused as follows:

- Green Future Focus (Greener) - Ambition to be the first carbon negative region - contributing to the Government's ambition to be net zero.

- People and Places Focus (Fairer) - Ambition to reshape and transform our places and ensure our people have great opportunities - contributing to the Government's Levelling up agenda

- Sector Focus (Stronger) - Ambition for a stronger, innovative and more productive economy - contributing to the Government's ambition of a Global Britain.

These are initial thoughts, but will be developed further with strong ambitious targets and outcomes.

4.4 Initial discussions and analysis undertaken as part of the LIS evidence base and the impact of Covid-19, have led to a series of sub-objectives or priorities being identified. Further research and discussions with stakeholders will now take place to develop these further but the initial ‘themes’ identified include the following:

Sector Focus

- Bio-economy

- Innovative Agri and aquaculture

- Advanced food manufacturing

- Visitor/cultural and creative economy

- Rail and transport technology

People and Place Focus

- Coast

- York

- Towns/rural

Greener Focus

- Natural Capital

- Circular economy and energy

4.5 Within each of these themes, the investment plans will be derived through identifying 'what investment is needed' in terms of:

- infrastructure

- innovation

- skills

4.6 To help this Plan for Growth underpin the principles of good growth, we would also look for the plan and investments to be aligned and contribute to the UN Sustainable Development Goals. This will support identifying defined outputs and measures for the plan.

The 17 UNSDGs are:

Further work will be undertaken regarding these as part of the Plan development.

Stakeholder engagement

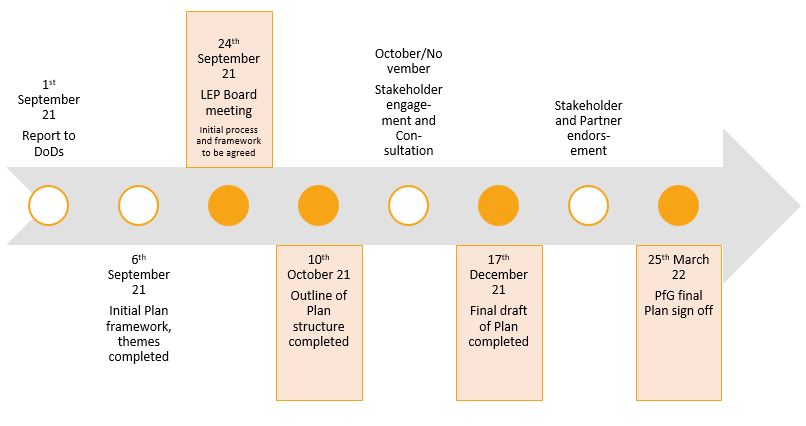

4.7 Stakeholder and partner engagement and consultation forms a critical part of the process for developing our Plan for Growth. It is proposed that this is undertaken at different stages of the Plan’s development. The first stage will be a series of round table ‘think tank’ discussions. These will be held in October and will provide some forward thinking and horizon scanning under a series of topic areas. These will be based around the initial objectives set out in this paper. Stage two will be a much wider engagement during October and November and will help to further develop the ambitions, priorities and actions or investments within the Plan. Finally, a further consultation and engagement process will be held in January and February to seek partner endorsement of the Plan.

4.8 Timeline

5. Recommendations

5.1 To note the contents of this report in the context of the process of developing a Plan for Growth for York and North Yorkshire

5.2 To receive further reports at subsequent meetings regarding progress.

Report author:

James Farrar, Chief Operating Officer, York and North Yorkshire Local Enterprise Partnership.

[1] Other Service Activities includes the activities of membership organisations, the repair of computers and personal and household goods and a variety of personal service activities not covered elsewhere in the classification.

[2] https://www.simplybusiness.co.uk/downloads/simply-business-report-covid-19-impact-on-small-business.pdf